This is the year I’m going to save more money. This is the year I’m going to take that dream vacation. This is the year I’m going to buy a house.

Studies have shown that most resolutions rarely last longer than a month. And chances are by now, in mid-January, the ambiguous goal of “saving more money in 2017” has likely started to slip to the bottom of the list, while financial obligations continue to quietly pile up.

Renowned financial expert, #1 New York Times bestselling author, and CreativeLive instructor David Bach states that “making a budget in order to save money is quite possibly one of the worst approaches to financial resolutions you could make.” Leveraging his experience of over 20 years as a financial advisor, and delivering seminars to millions of people seeking financial help, he has proof that “making a budget” is truly a flawed approach to financial freedom.

So what can people do differently in 2017 to achieve financial freedom?

In his book, The Automatic Millionaire, he shows us the way ordinary people can build an extraordinary wealth is – not to make a budget – but rather automate the process so you can literally build wealth while you sleep.

David Bach shared eight money-saving tips that you can do right away to help you achieve your financial goals in 2017:

Step 1: Be selfish about your income. You’ll be working approximately 2,000 hours in 2017 and around 90,000 hours in your lifetime. That’s a lot of time spent on the job, and unfortunately, less than half of the American population are happy with their jobs. Let 2017 be the year you make a decision to be passionate about the work you’re doing and be selfish about your income.

Step 2: Pay yourself first (at least one hour of your income per day). When you earn a dollar, the first person that should be paid is you. However, the way the American system of money in America is setup is that that Uncle Sam gets your money first (federal taxes, state taxes, social security) and then the next part of your income goes towards living expenses (housing expenses, food, transportation, etc). The first person that needs to get paid first is you. What does that mean exactly? Let’s break down a typical 9-5 work day and see where our paychecks go hour by hour:

In his book, The Automatic Millionaire, he shows us the way ordinary people can build an extraordinary wealth is – not to make a budget – but rather automate the process so you can literally build wealth while you sleep.

David Bach shared eight money-saving tips that you can do right away to help you achieve your financial goals in 2017:

Step 1: Be selfish about your income. You’ll be working approximately 2,000 hours in 2017 and around 90,000 hours in your lifetime. That’s a lot of time spent on the job, and unfortunately, less than half of the American population are happy with their jobs. Let 2017 be the year you make a decision to be passionate about the work you’re doing and be selfish about your income.

Step 2: Pay yourself first (at least one hour of your income per day). When you earn a dollar, the first person that should be paid is you. However, the way the American system of money in America is setup is that that Uncle Sam gets your money first (federal taxes, state taxes, social security) and then the next part of your income goes towards living expenses (housing expenses, food, transportation, etc). The first person that needs to get paid first is you. What does that mean exactly? Let’s break down a typical 9-5 work day and see where our paychecks go hour by hour:

Step 5: Find your Latte Factor®. A common complaint I hear is that people believe that they don’t have enough money to save even $10/day. For just two days only, take a close look at your daily spending habits and you’ll find that it’s easy to find $10 per day (such as from your daily latte or muffin).

Another way to do this is by using a tool like Mint.com for 30 days and take a close, hard look at where your money is going. After tracking 30 day’s worth of spending, look at your “Double Latte Factor®” and find out where money is being automatically deducted from your account from things like Netflix or your gym membership. When you pay someone automatically, these payees are on your “payroll” every month.

For example, a leased car that costs $400 per month vs. $600 per month might seem like a small difference month over month, but over the year this is additional $2400. Did you know 75% of luxury cars are leased and the bulk of cars are leased by people who don’t have that net worth? Look at who is attached to your “payroll” and get them off or make sure they fall within your annual and long-term budget.

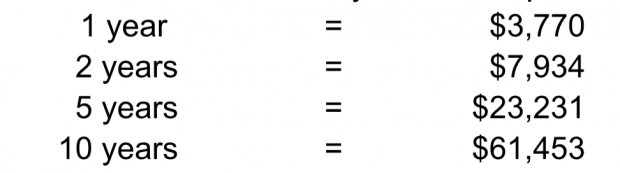

Not convinced you can earn 10% annually? Run your own calculation on our Latte Factor® Calculator and pick a lower return that makes your comfortable: https://davidbach.com/latte-factor/.

Step 6: Make this the year you love to fix your credit score. People can check their credit score every 12 months at sites like annualcreditreport.com to get one free credit report from each credit reporting company. You should know what your credit score is because the higher your credit score is, the less it costs to borrow money. And guess what, in just six months, there is a lot you can do to correct your score. Here are a few things for starters:

Step 5: Find your Latte Factor®. A common complaint I hear is that people believe that they don’t have enough money to save even $10/day. For just two days only, take a close look at your daily spending habits and you’ll find that it’s easy to find $10 per day (such as from your daily latte or muffin).

Another way to do this is by using a tool like Mint.com for 30 days and take a close, hard look at where your money is going. After tracking 30 day’s worth of spending, look at your “Double Latte Factor®” and find out where money is being automatically deducted from your account from things like Netflix or your gym membership. When you pay someone automatically, these payees are on your “payroll” every month.

For example, a leased car that costs $400 per month vs. $600 per month might seem like a small difference month over month, but over the year this is additional $2400. Did you know 75% of luxury cars are leased and the bulk of cars are leased by people who don’t have that net worth? Look at who is attached to your “payroll” and get them off or make sure they fall within your annual and long-term budget.

Not convinced you can earn 10% annually? Run your own calculation on our Latte Factor® Calculator and pick a lower return that makes your comfortable: https://davidbach.com/latte-factor/.

Step 6: Make this the year you love to fix your credit score. People can check their credit score every 12 months at sites like annualcreditreport.com to get one free credit report from each credit reporting company. You should know what your credit score is because the higher your credit score is, the less it costs to borrow money. And guess what, in just six months, there is a lot you can do to correct your score. Here are a few things for starters:

In his book, The Automatic Millionaire, he shows us the way ordinary people can build an extraordinary wealth is – not to make a budget – but rather automate the process so you can literally build wealth while you sleep.

David Bach shared eight money-saving tips that you can do right away to help you achieve your financial goals in 2017:

Step 1: Be selfish about your income. You’ll be working approximately 2,000 hours in 2017 and around 90,000 hours in your lifetime. That’s a lot of time spent on the job, and unfortunately, less than half of the American population are happy with their jobs. Let 2017 be the year you make a decision to be passionate about the work you’re doing and be selfish about your income.

Step 2: Pay yourself first (at least one hour of your income per day). When you earn a dollar, the first person that should be paid is you. However, the way the American system of money in America is setup is that that Uncle Sam gets your money first (federal taxes, state taxes, social security) and then the next part of your income goes towards living expenses (housing expenses, food, transportation, etc). The first person that needs to get paid first is you. What does that mean exactly? Let’s break down a typical 9-5 work day and see where our paychecks go hour by hour:

- 9AM - 12PM - money earned goes towards paying taxes

- 12PM - 3PM - money earned goes towards living expenses

- 3PM - 5PM - money earned goes towards “other” expenses such as food, social activities, travel, misc.

Step 5: Find your Latte Factor®. A common complaint I hear is that people believe that they don’t have enough money to save even $10/day. For just two days only, take a close look at your daily spending habits and you’ll find that it’s easy to find $10 per day (such as from your daily latte or muffin).

Another way to do this is by using a tool like Mint.com for 30 days and take a close, hard look at where your money is going. After tracking 30 day’s worth of spending, look at your “Double Latte Factor®” and find out where money is being automatically deducted from your account from things like Netflix or your gym membership. When you pay someone automatically, these payees are on your “payroll” every month.

For example, a leased car that costs $400 per month vs. $600 per month might seem like a small difference month over month, but over the year this is additional $2400. Did you know 75% of luxury cars are leased and the bulk of cars are leased by people who don’t have that net worth? Look at who is attached to your “payroll” and get them off or make sure they fall within your annual and long-term budget.

Not convinced you can earn 10% annually? Run your own calculation on our Latte Factor® Calculator and pick a lower return that makes your comfortable: https://davidbach.com/latte-factor/.

Step 6: Make this the year you love to fix your credit score. People can check their credit score every 12 months at sites like annualcreditreport.com to get one free credit report from each credit reporting company. You should know what your credit score is because the higher your credit score is, the less it costs to borrow money. And guess what, in just six months, there is a lot you can do to correct your score. Here are a few things for starters:

- Make sure there aren’t any mistakes. It’s not uncommon to find mistakes on your credit report, from incorrect addresses to a payment you’ve made, but it’s showing up as unpaid. If there are errors, you need to contact the credit reporting company and have those mistakes repaired.

- Automate your bill paying. Nothing hurts credit faster than being late on a payment. Make sure you’re at least paying the bare minimum for your bills automatically. If you have had a missed payment, get current as fast as possible and within 6 months your credit score will go up.

- Keep your balance within your net worth. You should have only one card that’s being used and if you have other credit cards that you aren’t using, hold on to them and keep a zero balance because part of your credit score is based on how long you’ve had credit.

- Decide on a lender within 30 days. FICO looks at the number of inquiries. If you’re out shopping for a loan for 3 or 4 months, FICO will raise an eyebrow. Make sure to shop for a loan quickly within 30 days, because anything past that will be picked up by their algorithm and be a ding against your credit.